At present, we find ourselves facing an economy with absolutely unprecedented dynamics. In an incredibly short period of time, we went from:

- There’s a virus overseas that seems pretty nasty, to

- It’s coming here and we should cancel major events and take some pretty serious precautions, to

- Everything is shut down and we may be looking at another great depression.

This is truly like nothing we’ve ever seen before.

Here I try to discuss some of the themes I see emerging and how we might look at them as investors.

Before I dig in, a couple of points need to be made so that you can maximize the benefit from these ideas.

Leave Politics at the Door

First, understand that I simply don’t care about your politics. As far as this article goes, my interest in politics starts and stops within the bounds of how it impacts my ability to preserve or generate wealth. It’s impossible to discuss some of these themes without creating some political undertones. I don’t intend to vote this year, and I think the Rs and Ds are both ridiculous.

There, I said it. Don’t come at me with any partisan nonsense in the comments.

Generating an Investment Thesis

Next, it’s important to outline my broader mindset on investing and decision-making. I completely stole my investing mindset from people I know and look up to who are way smarter and wealthier than I am.

The wrong way to think about investing is deciding what you think will happen, putting all of your life savings into a couple investments that align with that idea, and then stubbornly sticking to it no matter the outcome.

The right way to think about investing in this climate is to understand the rapidly changing dynamics and to maintain flexibility. To be ready to strike when you see opportunities, and not be afraid to change your mind. Confront your biases and be ready to adjust course many times.

Generate a process that incorporates what you know and the relative probabilities of a given outcome. Constantly absorb new information and take everything you know into account to adjust and tweak your process as you navigate your investments. Stick to your process with discipline, and make the best decisions you can with the information you have.

Understand that we’re all guessing about this stuff. The more information, knowledge, and experience you have, the better the guess. But it’s always a guess, and I don’t pretend to have all the answers.

I could be wrong about all of this. I don’t pretend to have a crystal ball or to know exactly what is going to happen. But with the right investment process, I can put some money to work that stands to do well in any environment, while leveraging myself to the broader macro themes in place and minimizing my downside risk.

Make sense?

What We Know So Far

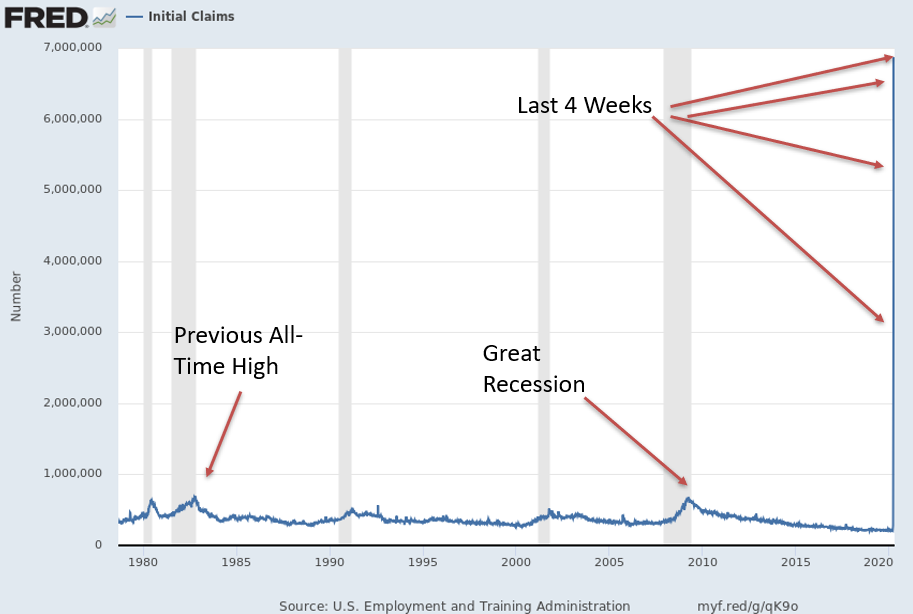

What we’ve seen up to this point is a very rapid wave of layoffs that has dwarfed prior periods. The initial jobless claims that came out Thursday showed the fourth consecutive week of record unemployment filings, bringing the total to 22 million people filing for jobless benefits.

For context—in 1982, the previous one-week record was set (data only goes back to the late 1960s) at about 640,000 million claims. With the weekly average over four weeks over 5 million, this is about eight times worse than the next worst episode since at least 1967 and likely since the great depression.

Estimates are still wide-ranging regarding how high unemployment will reach and how fast it will bounce back. Right now, very smart people from very prestigious organizations are projecting anywhere from approximately 15 percent to 32 percent unemployment at its peak. The worst reading on record for this metric is 24.9 percent, at the depths of the Great Depression.

There are still more questions than answers at this point, but what we do know is that economic activity has come to a screeching halt. The question becomes how soon and how vigorously does it bounce back?

The “V-Shaped Recovery”

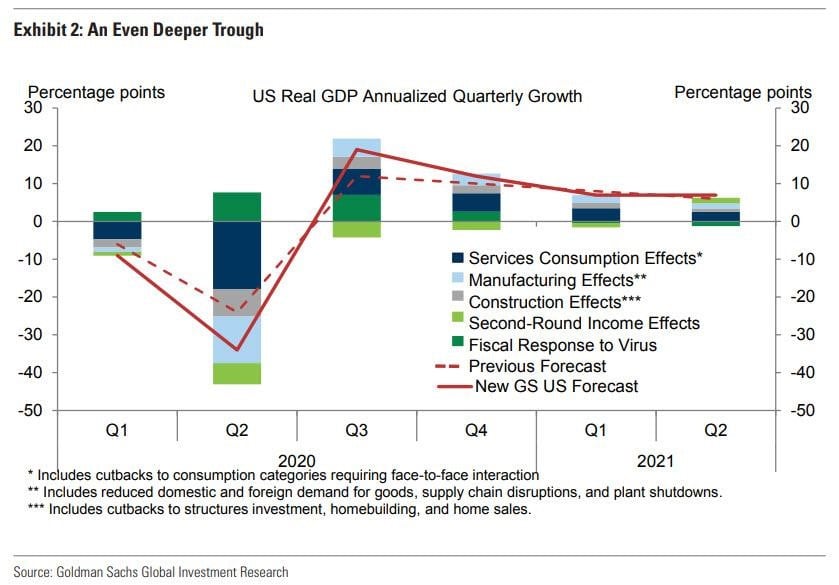

There is a chance that we’re looking at a quick bounce-back to a strong economy. Goldman Sachs came out with some estimates for GDP that largely support this idea.

Here they show a 9 percent GDP decline in Q1, a 34 percent decline in Q2, then an immediate 19 percent increase in Q3. The full 2020 projection is now calling for a 6.2 percent GDP decline, driven by the heavy Q2 decline and a sharp re-acceleration.

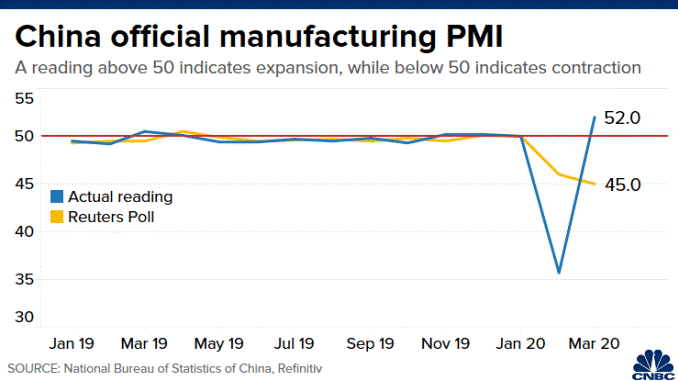

Looking at China may also provide support for the “V-shaped” recovery thesis.

It is important to note that the PMI above 50 signals expansion from the previous month, which was quite a low base to grow from and doesn’t signal that manufacturing is back to pre-virus levels. Also, there may be a shorter-term bump in Chinese manufacturing as Americans and Europeans first show increased demand to build stockpiles, only to have longer-term demand fall as the effects of unemployment are felt in the West.

This would be reflected in the China PMI in future months. There are also those who have a general mistrust in economic data out of China due to concerns that the government controls the data to a greater extent than the west.

Further supporting a quick recovery, we’ve heard from companies on the ground in China that they are getting back to business. Starbucks and Yum Brands (KFC, Taco Bell, Pizza Hut) are among the companies saying they’ve gotten nearly all restaurants re-opened in China.

In this scenario, there is a ton of pent-up demand building in the economy right now, and when the all-clear is signaled, America will come back with a vengeance. Businesses will hire, consumers will spend, and the recovery in jobs will match the velocity of the downturn. This is certainly a possibility, but we’ve got to think through some other potential paths, as well.

A Darker Path

The other path we may go down looks a bit more ominous. Understanding this scenario starts with thinking about credit cycles and whether we’ve kicked off the unwinding phase of the credit cycle that started as the last recession ended.

During the last crash, the Federal Reserve embarked on a program of zero interest rate policy (ZIRP) and quantitative easing (QE) that, at the time, seemed like a crazy amount of intervention. After recent Fed moves, it looks like child’s play. We can avoid a discussion for now as to the efficacy or judiciousness of the program, but it certainly had some effects of which we’re feeling today.

One of those effects was to encourage a great deal of borrowing—far more borrowing than what would have occurred otherwise. Businesses were able to become over-dependent on leverage, first for survival and later for enhanced profits.

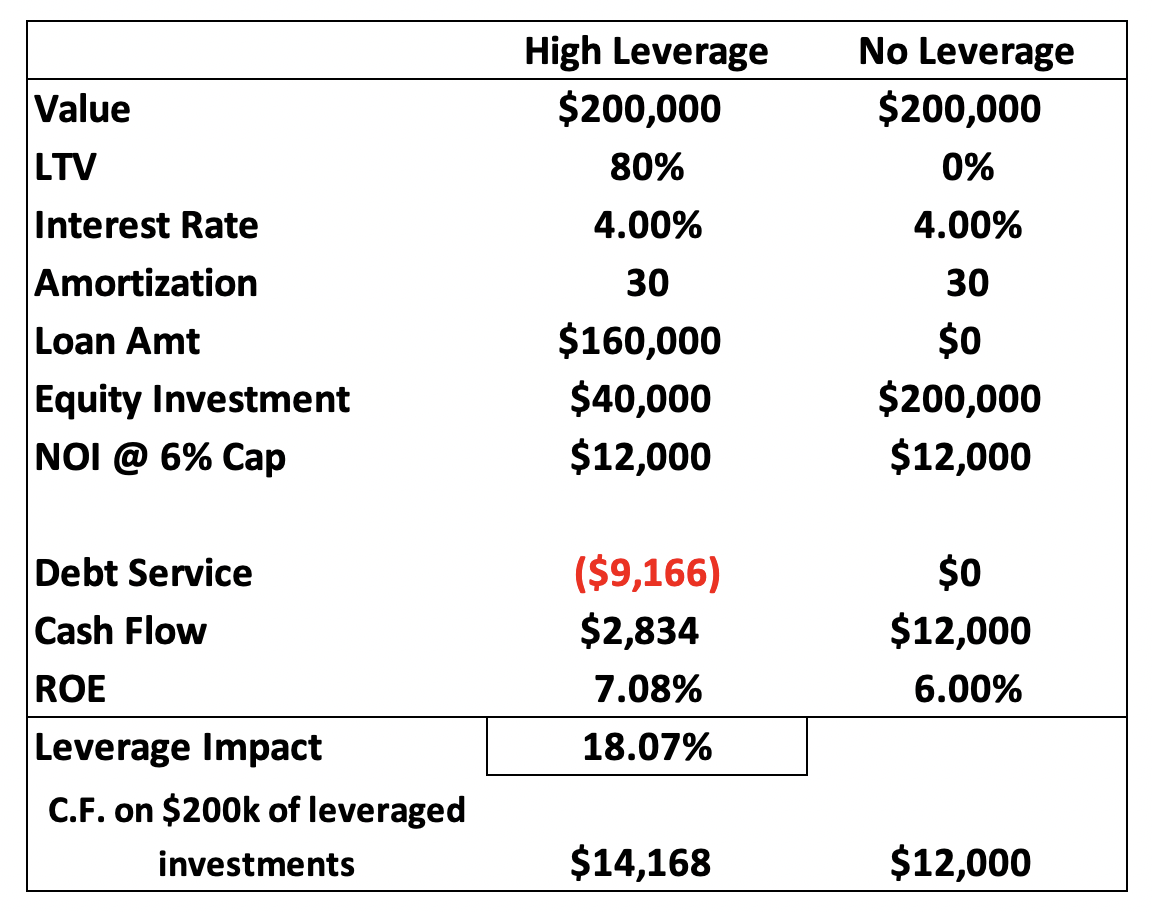

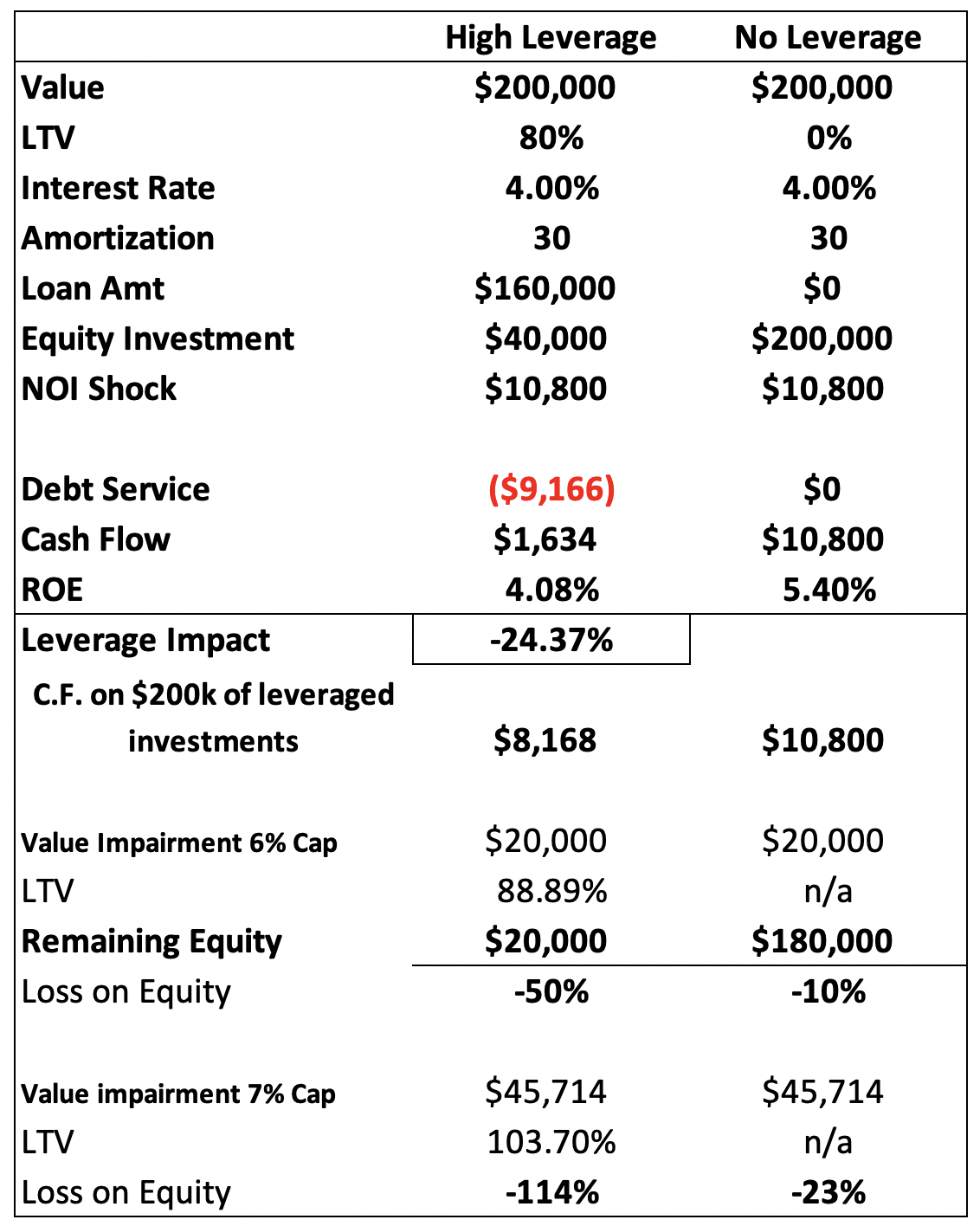

When you have a higher mix of debt relative to equity, your returns are higher. But you’re also taking on more risk. Disruptions to cash flow can put you out of business. Quick example:

Here we see that using 80 percent leverage on a real estate deal with some simple assumptions creates equity returns 18 percent higher than without debt. Also note that if you had $200,000 to invest, you could do five deals at 80 percent leverage but only one deal all cash. So you’re also generating about $2,000 more in cash flow. Seems like a no brainer, right?

But what happens if there’s a 10 percent shock to NOI? Might 20 or 30 million freshly unemployed people, who are likely disproportionately renters, have such an impact on a real-life investment?

Same investment, same NOI decline, CRUSHING difference on returns and value. Assuming the original 6 percent cap value holds, you’ve lost 50 percent of your investment and your LTV is higher than any bank will refinance. You’re now a forced seller.

Assume cap rates go up 100 basis points during a downturn (pretty reasonable, no?), and you’ve lost more than 100 percent of your investment.

With no leverage, you’ve missed out on some of the good times, but now you’re riding out the storm. You could even add some leverage now if you needed some cash.

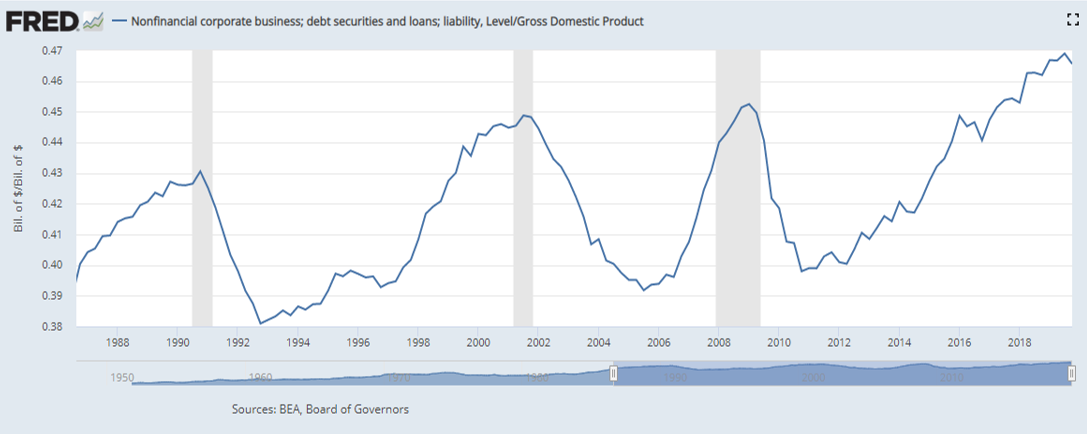

Now apply this concept to the entire U.S. economy! Corporations across the spectrum of industries were gorging themselves at the trough of low interest rates, leading to the highest corporate debt/GDP ratio ever recorded.

Much of this new debt was distributed to stockholders or used to buy back stock, not necessarily to increase the asset base and generate long-term cash flow.

Another effect of QE and ZIRP was moral hazard. Signaling that the government was ready to jump in and bail out companies that are “too big to fail” sent a message that additional risks could be taken because there is an implicit government backstop.

If declining revenue and a deleveraging cycle has started, we may be looking at a slower, tougher recovery.

We may see demand bounce back, but will all consumers (even the jobless ones) immediately bring their spending, vacations, events, etc. back to their previous levels? Will businesses hire everyone back immediately or reassess the new landscape and only rehire slowly and carefully? Will renters put more of an emphasis on scaling back and budgeting and less on having the best amenities and newest units?

Will $1,200, competing with auto loans, student loans, credit card debt, and other bills be sufficient to carry people through? Is it likely that the “quarantine” extends past April 30th?

These are the questions we must think through to determine which path we’re on.

I believe financial markets, real estate, and the broader economy was on a bit of a shaky footing before this started. I hope it’s just my natural bias toward risk aversion kicking in here and that we rebound sharply, but in my gut, I feel like this scenario may be more probable.

Let’s dig into some new or growing themes that I think will impact the investing landscape for the next several years—or even decades.

Capitalism Is Dead: Long Live the Central Bank

I’d argue capitalism got terminally ill in 1913. The disease metastasized in the 1930s. It went into hospice in 1971 and flat-lined in 2009. Now the doctors have finally pronounced it. Time of death: March 2020.

It’s a new way of life. Central banks around the world have created a situation where they’re holding a wolf by the ears. They can’t hold on forever, and they can’t let go. Their only strategy is to try and prop things up with more and more debt, each time needing a more massive program to avoid a painful but necessary restructuring of the economy.

Bailouts and stimulus from the congress will likely follow a similar trajectory. No one wants to look like the guy who didn’t do anything.

If we’re going to invest our money properly, we’ve first got to accept the fact that we can’t rely on free-market ideas or mechanisms to play out. We’ve got to figure out how to navigate a world with no real price discovery in capital markets, bailouts, moral hazard, private profits but socialized losses, and a manipulated and devalued currency.

Tack on the regulatory situation, lobbyists, and the tax code, and I’m not sure what we should call our current economic system. But it sure as hell isn’t capitalism.

Bailout Nation

I think a bailout of state and local pension systems will be on the docket in short order. Many of these were drastically underfunded after a 10-year expansion with sky-high stock prices. They have no chance of keeping their promises to retirees after a stock market correction.

Will these states and municipalities be able to raise taxes drastically in the midst of a recession to fund these pensions? Doubt it. Their best bet is to appeal to the federal government for a bailout. Will the federal government raise taxes? Nope. Money printer go brrr.

Further bailouts of over-leveraged corporations? Bailouts of banks because they’ve suspended mortgage payments? Bailouts of landlords? Bailouts of hospitals after they eliminate COVID-19 patients’ medical bills? It’s all possible now.

Who pays for all the bailouts? We do. The future economy does in slower growth, through higher taxes, higher inflation, less efficient businesses, and capital flowing to Washington and crowding out the private sector.

Inflation Is Coming

Maybe not today, maybe not tomorrow, but it is coming.

The Federal government is already insolvent for all intents and purposes. So are many state governments (looking at you, Illinois). If they were required to list all of their future obligations for pensions, Social Security, and Medicare, it would be pretty obvious that we would need to see massive tax hikes and massive cuts to spending for them to remain solvent.

Would any politician keep their job proposing such ideas?

There is one alternative that is much more attractive to politicians, especially with the backdrop of current central bank policy. They can default nominally without having to actually default by monetizing the debt. The Treasury will issue bonds to pay for everything, and the Fed will buy them up by creating bank reserves and base money (printing money, as it is generally referred to in the media).

We had $1 trillion deficits before this mess. We added another $2 trillion to the debt in a heartbeat this weekend. How bad is the deficit going to get when tax revenues fall off a cliff and unemployment and other assistance surges?

Does anyone in their right mind think the ability, or even the political will, exists in Washington D.C. to raise people’s taxes to the level required to pay this debt? Or to cut spending?

The only realistic option is for the Fed to monetize the debt. We’ll still pay for it, just through inflation and not taxes. Money printer go brrr.

I think onshoring or re-shoring will become a theme over the next few years, which is broadly inflationary, as well. More on that below.

How about when the next wave of fiscal “stimulus” comes through? I think we’re going to start seeing an obscene amount of “stimulus.” Airports, roads, bridges, bullet trains, you name it. Now is the chance for all of the politicians to get their pet projects through Congress while everyone is afraid and vulnerable. Very inflationary.

The question on inflation is a matter of when, not if. When will the deflationary impacts of this recession become outweighed by the massive money creation and fiscal deficits? When will people lose faith in the government’s ability to pay off its obligations?

When that happens, bond holders will sell off treasuries and the Fed will have to step in with more QE to keep the rates low. But this will create a negative feedback loop. More printing > less confidence in currency > sell treasuries > higher rates > more printing to keep rates down.

Geopolitics, Energy Independence, and Onshoring

The U.S. dollar has long been the reserve currency facilitating international trade. This has been a major factor explaining why inflation hasn’t picked up as much as some have predicted. There is a constant demand for dollars from other countries as they view it as the most stable, liquid, and trustworthy currency in which to trade goods.

If my take on money creation and inflation is correct, there is going to be intense pressure on many countries to find alternate currencies for transactions. I would look toward Russia and China as likely culprits in a sprint for alternatives. This process has been underway for a few years already, but now it will accelerate.

We may see gold and gold backed currency reappear in the world. Cryptocurrency may also begin to play a more meaningful role in international trade.

The geopolitical situation was already shifting with trade wars and tariffs. That’s going to go into hyperdrive now. The Saudis, often viewed as American allies, picked an interesting time to declare war on U.S. shale oil. Russia is playing a major part in this, as well.

American shale oil is more expensive to produce than oil from the Middle East and Russia. These companies can’t survive long with $20/barrel oil. It will be interesting to see what the U.S. policy response will be and if any assistance will be provided to U.S. shale.

Without shale, the idea of U.S. energy independence likely goes out the window. This turns the entire geopolitical landscape on its head.

Lastly, I think onshoring will be a theme to watch for in the coming years. Companies are beginning to realize that there are some pretty large risks to having their supply chains originate in one place, halfway across the world in an authoritarian country. I think there is going to be pressure, corporately and politically, for companies to bring some manufacturing capability back on shore.

How to Play It

So, what does it all mean for us, those trying to figure out how to make some money in these crazy times?

Remember the first rule of investing. Never listen to a guy on the internet.

What I’m thinking about doing is a three-pronged approach.

First, I’m looking at some inflation hedges. I’m thinking about how much of my portfolio should be allocated to gold and in what form. Physical, ETF, stocks of gold companies? I’m going to start actually educating myself about Bitcoin and other crypto, which I’ve largely stayed away from mostly because I didn’t have the energy to try to understand it.

Second, I’m looking at high-quality companies with strong balance sheets that pay good dividends. I think there’s a good chance the bottom isn’t in on the stock market yet, but making a list of these companies so that I’m ready to strike makes sense. Picking the bottom is impossible but for blind luck, so buying little by little on down days may be a good strategy.

Lastly, real estate is where I’ll really butter my bread. Properly constructed, real estate can be a great investment in periods of inflation, because your rents can inflate alongside your expenses while your debt payment remains fixed. The government is going to inflate the currency so they can pay off their debts with less valuable dollars. We might as well piggyback off of that as well and borrow money at today’s low rates to buy some great real estate deals. (Just please remember the danger of over-leveraging as described above.)

For this, I want to focus on high-quality, in-demand property with long-term, fixed-rate debt. I like Class A- and B multifamily and self-storage. Maybe some high-quality industrial tenants with good credit, provided there are inflation escalations in the lease. Special attention, for now, should be paid to which industries are dominant in a given area and understanding the employment profile of tenants.

Market Dynamics

What we’re seeing so far is that sellers aren’t moving off their pricing expectations by much. It seems like they’d rather hold out or pull their deals off the market and wait for now, so we may simply have a slow market without many transactions.

However, if it begins to look like the economy is moving down the more pessimistic path, many sellers may rush for the exits to preserve their values while they can.

Nationwide, there are around 500,000 apartment units scheduled to be delivered over the next several quarters, right into the teeth of the jump in unemployment and a general shift in renter preferences toward lower rents and more value. We may be looking at some longer-term vacancy issues and sluggish rent growth.

Buyers that are up against debt maturities or that overpaid for deals recently may become motivated sellers.

This may be the time to start thinking about the early planning stages for buying distressed properties and looking for great deals in some of the old channelsâloan servicers, banks, direct from struggling sponsors, etc.

About a year ago, I penned an article here on BiggerPockets titled “March Madness! Yield Curve Inverts and the Fed Throws in the Towel.” I think my advice then is still sensible now. We have two options:

- Keep calm and carry on. Look for the right deals. Use lower leverage. Sell marginal deals. Raise some cash, so you can take advantage of a down market.

- Make a hat out of tinfoil. Buy 100 acres in northern Wisconsin. Do bug-out drills and practice eating worms.

I think I know which option I’ll choose. See you in the woods!

Article by By Phil McAlister from Bigger Pockets.