On March 11, 2020, the World Health Organization (WHO) officially designated the coronavirus and COVID-19 (the respiratory illness it causes) a pandemic. Cases have occurred in 114 countries and resulted in approximately 120,000 infected people and more than 4,000 deaths.

Although the statistics and the ways the illness affects individuals’ lives are rapidly changing, we’ve taken a look at how the outbreak is impacting U.S. domestic real estate markets up to this moment.

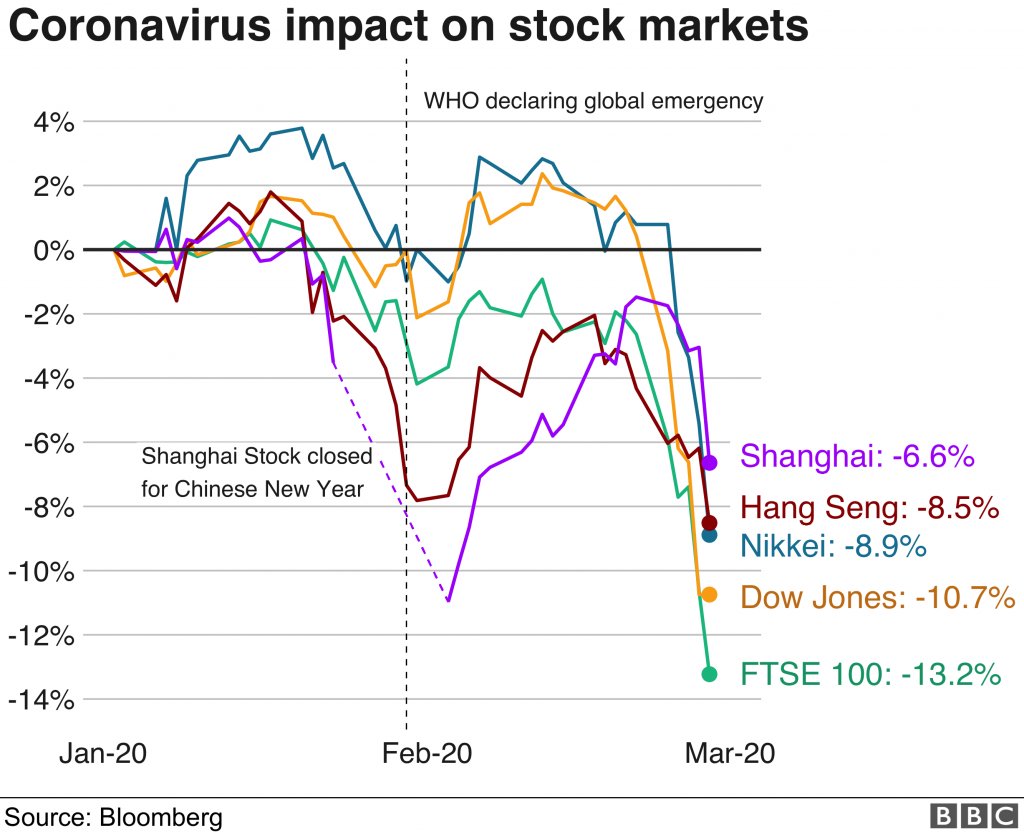

A Summary of Related Economic Events

Since the WHO declared a global emergency on Feb. 20, 2020, major stock indices around the world have dropped an average of more than 9 percent. The Dow Jones Industrial Average suffered its largest single-day drop in history on Feb. 27, 2020.

- The travel industry is sustaining significant losses. Major conventions are being canceled, and large companies are discouraging non-essential travel. More than one-third of business travel in 2020 may be lost.

- On March 15, 2020, the Federal Reserve cut its benchmark interest rate to 0 percent and announced plans to buy at least $700 billion in government and mortgage-related bonds. This happened less than two weeks after the Fed cut the benchmark rate by 50 basis points to just below 1.25 percent.

- On March 6, 2020, Congress passed a bipartisan $8.3 billion coronavirus bill that includes $3 billion for developing coronavirus treatments, $2.2 billion to help stop its spread, and more than $1 billion to aid efforts overseas.

- Mortgage rates have dropped to three-year lows, to approximately 3.5 percent at the time of this post.

- Overall U.S. growth may drop to below 2 percent in the first quarter, and lost global output due to the virus could amount to $2.7 trillion.

- On March 13, 2020, President Trump declared a state of emergency, which is expected to make $40-50 billion available to address the outbreak.

Will Economic Volatility Caused by Coronavirus Impact Real Estate?

Despite what many people believe, there isn’t a direct connection between stock market performance and real estate values. It’s the overall health of the economy (which prior to the events of the past two weeks, was still considered relatively strong) that ultimately affects them both. As long as consumers feel confident about their jobs and income, they will continue to spend—and that includes buying real estate.

Among other things, the strength of the real estate market is impacted by treasury bond prices, which are correlated to mortgage rates. When the stock market and other asset classes start to see a lot of volatility, investors will move their cash to bonds for stability and security. As demand for treasury bonds increases, however, bond prices go up and their yields (the interest they pay investors) fall. And that pulls mortgage rates down, too.

It’s worth noting that the catalyst for today’s economic situation is very different from the 2008 financial crisis, which was directly caused by issues in the sub-prime lending market. During that recession, sub-prime mortgages were bundled up and sold for much more than they were worth. Ultimately, real estate speculators let homes financed by these mortgages go into default, and these bundles of mortgages—called credit default swaps—lost most of their value, bankrupting large investors and starting a domino effect that rippled through all aspects of the economy.

The current stock market volatility is not the result of issues in the real estate market, but is specifically the result of uncertainty about how the coronavirus may impact supply chains and corporate earnings. While it remains to be seen, real estate may be insulated to some extent because of tight residential inventory, high buyer demand, low mortgage rates, and lower prices for lumber and oil.

But this is a continually evolving story. As of this writing, 10 states have ordered everything from mandatory shutdowns of all non-essential businesses to limits on restaurants, only allowing delivery and take-out options. Everything from Broadway to Disney World to Colorado ski resorts are at least temporarily closed, and discretionary travel has for the most part stopped.

While the businesses involved may (or may not) have the resources to survive these conditions, there is no doubt that employees will be immediately and directly affected. Not only are their hours and income suddenly in jeopardy, but their jobs may go away. And this will impact real estate markets.

When people start to lose their jobs and see their hours and wages cut, their disposable income drops. This results in their spending less money, one of the most important factors in maintaining the health of the economy. A reduction in spending directly (and negatively) affects U.S. GDP, unemployment, and income growth—all of which are needed to support housing prices.

In other words, if employers see long-lasting decreases in revenue, they will start laying off employees, and their laid-off workers will have less to spend—which slows growth further and creates a vicious cycle leading to more layoffs. This would affect housing markets by tipping the current balance of low supply and high demand.

Savvy investors should keep a close eye on these developments, as well as continue to track mortgage interest rate changes and any government stimulus packages enacted to help ease the impact of coronavirus on the overall economy.

What About a Recession?

By definition, two successive quarters of declining GDP officially represents a recession, and recessions always have significant impact on individuals’ incomes. Reduced income and wages results in homebuyers and renters having less to spend on their monthly housing costs, leading to lower home prices and lower market rents.

It’s worth noting that we might already be in a recessionary period (we won’t know until today’s economic data is released a couple months from now). In addition, Goldman Sachs has forecast significant declines in U.S. GDP from now through June. And UCLA Anderson School of Management’s Anderson Forecast says that the economy has stopped growing and won’t recover until the end of September.

It’s still early in this crisis, but we expect hospitality-related real estate markets to experience the most immediate impact. Hotels, for example, will probably not be able to recover lost revenue, and planned construction in this sector is likely to be put on hold for the foreseeable future. Airbnb properties will probably be hit very hard, because once customers start traveling again, they will be more wary of the cleanliness of privately owned homes compared to larger chains with professional maintenance and cleaning staffs.

The impact on commercial real estate remains to be seen. It’s a slower-moving, more stable market that responds much later than more volatile indicators like stock performance. Cushman & Wakefield notes that “if the virus has a sustained and material impact on the broader economy, it will have feed-through impact on (commercial) property…”

Commercial real estate is also comprised of many different asset classes—from office to retail to warehouse—and each of these asset classes may respond differently during the next economic downturn.

That doesn’t mean there’s no potential bright side to all this negative news. During three of the last five recessions, home prices actually went up—anywhere from 1.9 percent to 4.8 percent. And if the economic impact due to coronavirus follows the pattern set by past public health issues, we may be poised for a strong rebound once the virus is under control and normal activities have resumed.

Additionally, there may be other factors that may lead to more desirable outcomes. As mentioned earlier, low inventory and high demand may help prop up the real estate market through the crisis. At the end of last year, the number of homes for sale was down 9.5 percent annually and the number of entry-level homes was 16.5 percent lower than the year before. Realtor.com already predicts historic inventory lows this year.

What If Coronavirus Directly Impacts Your Investments?

Depending on how all these details and forecasts play out, you could find yourself facing unexpected investment challenges, like reliable tenants suddenly unable to pay rent. Lower income workers with little, or no, savings could feel the greatest financial impact as various venues and businesses cancel events, limit hours, or completely close their doors.

But at the same time, more and more municipalities are putting eviction moratoriums in place as the health crisis unfolds. The federal government is being pressured to enact a national moratorium. As of this writing, Los Angeles, Santa Monica, San Francisco, Miami, Philadelphia, and San Jose, California, Austin, Texas, and the state of New York have either put moratoriums in place or have temporary holds on processing evictions.

If these circumstances affect your ability to meet mortgage payments, the Federal Housing Finance Agency (FHFA) has advised mortgage servicers to offer forbearance options. These will allow borrowers impacted by COVID-19 and related safety measures (like quarantines and business closings) to take advantage of hardship forbearance.

Options include temporarily reduced or suspended mortgage payments for up to six months, although interest will accrue during the forbearance period. Arrangements often provide a reinstatement or repayment plan to make up missed payments.

Are There Any Positives in the Current Situation?

The most obvious bright spot in the current uncertainty is low mortgage rates. Since the Fed usually doesn’t move quickly to undo stimulus efforts, rates are likely to remain low for a while. If demand and consumer confidence remains high, that presents opportunities to refinance existing properties and to move forward on new purchases.

Jerry Padilla, a lender in Rochester, N.Y., says, “Investors are already looking to refinance their properties and to make purchases while rates are so low.” He adds, “Everyone seems to have a sense of urgency, but investors need to understand there will be delayed turnaround times as lenders are seeing huge influxes of business.”

Colin Smith, a Realtor in Colorado Springs, Colorado, says, “We’re seeing extreme competition among single-family homebuyers that we haven’t seen since 2017.”

Be aware that there are a couple of scenarios in which the new lower rates might not be helpful, such as if you’re underwater on the value of a property or in a fixed-rate mortgage that’s not high enough to justify the expense of refinancing.

Home equity lines of credit (HELOC) are expected to come down soon in response to the new federal funds rate. If you have already borrowed on a HELOC, this will lower your interest expenses. If you’ve been considering a line of credit, it may be time to investigate the best available rates in your area.

Summary

The coronavirus’s ultimate impact on real estate markets will largely depend on the length of the outbreak and whether there is a quick recovery (with a return to overall social and economic stability) or a more extended one (in which medical outcomes are worse than expected, and consumer and economic disruptions linger).

At the moment, residential investments are well positioned, largely due to aggressive action by the Fed, low mortgage interest rates, and an advantageous balance between supply and demand. This has already resulted in an increase in residential property values over the past several weeks.

But some experts say that a recession has already begun that could last through the next several quarters. In anticipation of decreased economic performance, the FHFA has advised mortgage servicers to offer forbearance options to mortgage holders facing financial difficulties related to the coronavirus and COVID-19.

As a prudent investor, stay focused on factors that could change the outlook. For example:

- Quarantines and social distancing will create slower revenue and growth in commercial real estate and may cause increases in defaults on commercial loans.

- Uncertainty around our future economic outlook may move some buyers to the sidelines (reducing demand) and may induce some sellers off the sidelines (increasing supply).

- According to Green Street Advisors, real estate investment trusts (REITs), usually safe havens during stock market declines, have been surprisingly hard hit by recent volatility.

- New construction projects could be delayed by supply chain disruptions or possible labor shortages.

- Travel and related industries could have a ripple effect as major air carriers make significant cuts to their schedules and begin to ask staff to take unpaid leave.

- Realtor Colin Smith reports that some of his lending resources have seen lack of activity on large blocks of mortgages for sale. If that becomes a trend, mortgage brokers could face difficulties generating capital for new business.

- Look to trusted sources like BiggerPockets for insights on how these many different considerations are influencing markets, public health, and important decision-makers.